Af en Senior B2B Sustainability Content Strategist

Den Europæiske Unions engangsplastikdirektiv (SUP) (direktiv 2019/904/EU), der blev vedtaget i juli 2021, repræsenterer et seismisk skift i miljøpolitikken med dybtgående konsekvenser for foodservicesektoren. Dette direktiv er langt mere end blot en lovgivningsmæssig opdatering, og det er et strategisk imperativ designet til at begrænse det omfattende problem med plastikforurening, især havaffald, som tegnede sig for op til 70 % af alt havaffald før SUPD's implementering. For indkøbsledere, driftsdirektører, bæredygtighedsansvarlige og forsyningskædeledere er SUPD ikke kun en overholdelsestjekliste; det er en opfordring til grundlæggende at revurdere sourcing, drift og langsigtet forretningsstrategi.

Ignoring the mandates of the SUPD is no longer an option. The operational and commercial impacts of non-compliance are severe, ranging from hefty fines and supply chain disruptions to significant reputational damage and the alienation of an increasingly environmentally conscious consumer base. Proactive adaptation is essential not just for legal adherence but for securing market access, enhancing brand value, and fostering sustainable growth in a rapidly evolving European landscape.

The EU SUPD is a strategic imperative for foodservice, demanding proactive adaptation for compliance and sustainable growth.

Understanding the Core Tenets of the EU Single-Use Plastics Directive

At its heart, the SUP Directive aims to accelerate the transition to a circular economy by targeting specific plastic items with high environmental impact. Understanding its definitions and bans is the first step toward effective procurement.

Defining Single-Use Plastics

The directive precisely defines single-use plastics as products made wholly or partly of plastic, including bioplastics like PLA, intended to be used only once or for a short period before disposal. This broad definition ensures comprehensive coverage, leaving no room for ambiguity regarding what falls under the regulation.

Outright Bans (Effective July 3, 2021)

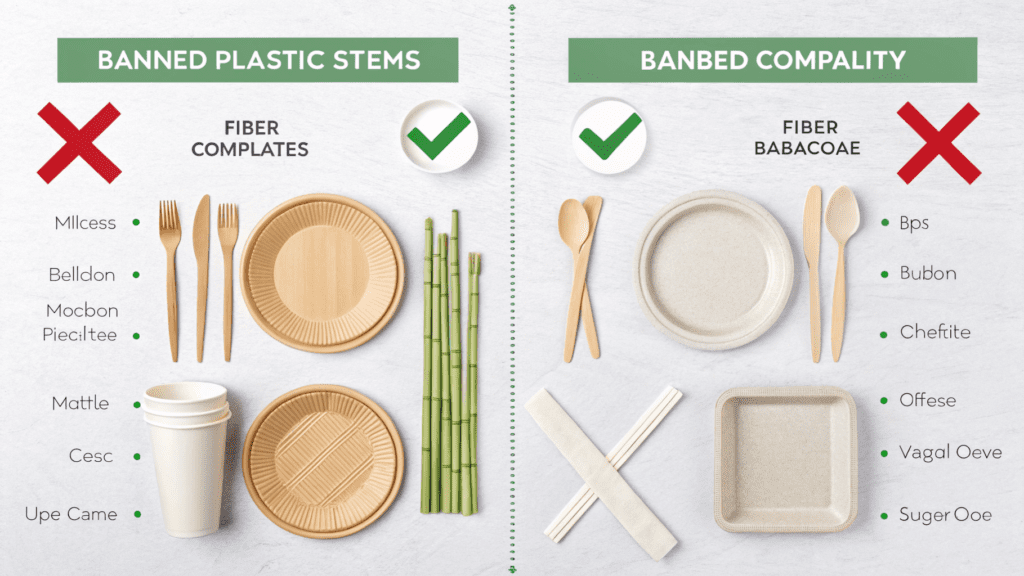

Den mest umiddelbare indvirkning på indkøb af madservice kom med det direkte forbud mod flere almindelige engangsplastikartikler. Siden den 3. juli 2021 har EU forbudt markedsføring af plastikbestik, tallerkener (selv dem med plastikforing som PE og PLA), sugerør (med undtagelser til medicinsk brug på hospitaler for patienter, der ikke er i stand til at indtage selvstændigt), drikkevareomrørere, bomuldspinde, ballonpinde og engangsfødevarebeholdere (EPS). Desuden er alle produkter fremstillet af oxo-nedbrydelig plast universelt forbudt i hele EU, hvilket afspejler en forpligtelse til virkelig bæredygtige alternativer.

SUP-direktivet er rettet mod højpåvirkningsplastikgenstande, hvilket nødvendiggør en klar forståelse af definitioner og forbud mod overholdelse af foodservice.

Direct Impacts on Foodservice Procurement: The Shift to Sustainable Alternatives

The outright bans necessitate an immediate and decisive material transition for foodservice businesses operating within the EU. Procurement teams must pivot away from traditional plastics towards a new generation of sustainable alternatives.

Immediate Material Transition

Businesses are now sourcing items made from materials such as unlined paper, molded fiber, bamboo, husk, bagasse/corn starch, and other plant-based materials like palm leaf or areca. This shift is not merely about finding a substitute but about integrating a new material philosophy into the entire supply chain. For example, considering options like innovativeKaffebanerstråcan help businesses meet sustainability goals while offering unique customer experiences.

Reduction Targets for Consumption (from 2023)

Beyond outright bans, the directive mandates that Member States quantitatively reduce the consumption of single-use plastic cups and takeaway containers. From 2023 onwards, countries must implement these reduction targets, using 2022 consumption levels as a baseline, aiming for “measurable quantitative reduction” by 2026. This requires not just material substitution but also strategies for waste reduction and potentially, a move towards reusable systems.

PFAS and Chemical Restrictions (by August 2026)

Landskabet for fødevareemballage kompliceres yderligere af den nye emballage- og emballageaffaldsforordning (PPWR), som tager sigte på "kemikalier for evigt". Senest den 12. august 2026 vil denne forordning forbyde per- og polyfluoralkylstoffer (PFAS) i fødevareemballager over 25 dele pr. milliard (ppb) til målrettet PFAS-analyse. Denne strenge grænse nødvendiggør en grundig gennemgang af alle barrierebelægninger og materialer i kontakt med fødevarer, hvilket skubber indkøb i retning af PFAS-frie løsninger for at undgå betydelige overholdelsesrisici.

Eliminering af plast til produktion (inden januar 2030)

The PPWR also extends its reach to fresh produce. From January 1, 2030, single-use plastic packaging for unprocessed, fresh fruits and vegetables weighing less than 1.5 kilograms (kg) will be prohibited, with limited exceptions for specific needs like mitigating water loss or microbiological hazards. This future ban requires foresight in agricultural supply chains and packaging development.

Foodservice procurement must transition to sustainable materials, meet reduction targets, and prepare for PFAS and produce plastic bans.

Evolving Compliance & Operational Shifts Under the EU Single-Use Plastics Directive

The SUPD’s influence extends beyond material composition, encompassing labeling, producer responsibility, and product design.

Mandatory Labeling Requirements (Since July 2022)

Transparency is key under the SUPD. Since July 2022, all disposable cups sold in the EU, even those with an aqueous lining, must carry a conspicuous, clearly legible, and indelible “Plastic in Product” or “Made of Plastic” turtle logo. This marking informs consumers about the plastic content, environmental impact, and proper disposal methods, directly influencing consumer perception and disposal behaviors.

Extended Producer Responsibility (EPR) Schemes (from December 31, 2024)

"Forureneren betaler"-princippet er en hjørnesten i SUPD. Fra den 31. december 2024 vil producenterne bære det økonomiske ansvar for indsamling, transport, behandling, oprydning af affald og bevidstgørelsesforanstaltninger for specificerede SUP-varer, herunder fødevarebeholdere, pakker, indpakninger, drikkevarebeholdere, kopper og letvægtsplastikposer. Disse EPJ-ordninger ændrer fundamentalt omkostningsstrukturen for emballage, hvilket gør bæredygtige materialevalg mere økonomisk attraktive i det lange løb.

Vedhæftede caps og genbrugsindholdsmål (senest juli 2024)

The directive also addresses product design to promote recyclability. From July 2024, plastic bottle caps and lids for beverage containers up to three liters must be attached to the containers, preventing them from becoming separate litter. Furthermore, demanding recycled content targets are set: PET bottles must contain at least 25% recycled plastic by 2025, increasing to 30% for all plastic bottles by 2030. This drives demand for recycled content and strengthens the circular economy.

Increased Collection Targets

To support these recycling goals, the directive sets ambitious collection targets for plastic bottles: 77% by 2025 and an impressive 90% by 2029. Member States are implementing various strategies, including deposit return schemes, to achieve these rates. Germany’s deposit return system, for example, already boasts a remarkable 98% collection rate for plastic beverage bottles, demonstrating the effectiveness of such schemes.

SUPD mandates labeling, EPR schemes, attached caps, recycled content, and higher collection targets, reshaping foodservice operations.

Strategic Procurement for EU Single-Use Plastics Directive Compliance

Navigating these multifaceted regulations requires a strategic overhaul of procurement functions.

Supplier Re-evaluation and Sourcing

Den umiddelbare opgave for indkøbsteams er at identificere og integrere leverandører, der tilbyder reelt overensstemmende alternativer. Dette indebærer en grundig undersøgelse for certificeringer (f.eks. industriel komposterbarhedsstandard EN 13432), materialesammensætning og forsyningskædens pålidelighed. Virksomheder skal sikre, at alternativer, som f.eksbæredygtige boba-halmalternativer, opfylder ikke kun lovmæssige krav, men opfylder også driftskrav og kundernes forventninger.

Omkostningsimplikationer af overgang

While the long-term benefits of compliance are clear, the initial transition can present cost challenges. Biodegradable or compostable products may initially be more expensive than their plastic counterparts. However, these upfront costs must be weighed against the significant risks of non-compliance, potential fines, and the long-term savings from reduced EPR fees and enhanced brand value. For instance, Poland has already applied additional fees on single-use plastics from January 2024 (e.g., PLN 0.20 for cups, PLN 0.25 for food containers) to cover waste management, illustrating the direct financial impact of non-compliance.

Optimizing Logistics and Storage

Shifting to lighter, more compact sustainable alternatives can offer unexpected benefits. These materials can reduce transport carbon footprint and optimize storage needs, leading to operational efficiencies and potential cost savings in warehousing and distribution. This optimization plays a crucial role in building a more agile and sustainable supply chain.

Mini Case Study: Xylomatrix’s PFAS-Free Innovation

A prime example of compliance-driven innovation comes from Xylomatrix, a company providing biodegradable cellulose fiber packaging. Their solutions offer crucial water and grease barriers without relying on harmful PFAS chemicals, directly addressing the upcoming PPWR restrictions. Such innovations highlight how businesses can not only comply but also lead the market with safer, more sustainable products, building trust and reputation. Many leading foodservice operators in Europe are already requiring certified compostable packaging, demonstrating a market-driven shift.

Comparison Table: Single-Use Plastics vs. Compliant Alternatives

| Feature | B2B operationel effekt | Overholdelsesnotat | ROI-potentiale |

|---|---|---|---|

| Single-Use Plastic Cutlery (PS/PP) | High waste volume; ongoing disposal costs. | ForbudtEU-wide since July 2021 (Directive 2019/904/EU). | Negative: Risk of substantial fines, severe reputational damage, consumer backlash, market exclusion. |

| Molded Fiber Plates (Bagasse) | Requires new supplier relationships; potentially higher unit cost. | Compliantalternative, widely accepted in EU; often industrially compostable (EN 13432). | Positive: Enhanced brand image, meeting growing consumer and regulatory demand for sustainability, potential for reduced waste management costs (e.g., compostability), long-term operational stability by proactively avoiding future bans. Supports circular economy goals. |

| Single-Use Plastic Cups (PET/PP lined) | Consumption reduction targets; labeling requirements. | Reduction targetsfrom 2023; “Plastic in Product” label since July 2022. | Variable: Non-compliance risks (fines, public scrutiny); opportunity for cost savings via reduction initiatives; improved brand perception. Strategic shift to reusable options can yield significant long-term savings and stronger loyalty. |

| Reusable Container Systems | Investment in washing/sanitizing infrastructure; logistics for returns. | Mandatedfor on-site by 2030; takeaway options by February 2028 (with no extra charge). | High: Significant long-term cost savings by eliminating recurring purchase of disposables, strong sustainability leadership, improved customer loyalty, potential new revenue streams (deposit schemes), reduced reliance on fluctuating material costs. Drastically lowers environmental footprint and positions business as a market leader in sustainability. |

Strategic procurement involves re-evaluating suppliers, managing transition costs, optimizing logistics, and embracing innovative, compliant solutions.

Embracing Reusable Solutions & Future Outlook for Foodservice Procurement

The SUPD and subsequent regulations clearly signal a strong push towards reusable systems, emphasizing a shift from single-use material substitution to systemic change.

Future Bans in HORECA (by 2030)

The trajectory of regulation is clear: by 2030, single-use packaging will be prohibited for certain foods and beverages consumed on-site at hotels, restaurants, and catering establishments. This extends to individual portion containers, such as creamers, sugar packets, and condiment sachets. This impending ban requires foodservice operators to invest in reusable crockery, cutlery, and condiment dispensers.

Customer’s Own Container Option (by February 2027)

To foster a culture of reuse, foodservice establishments will be required, by February 2027, to offer and actively inform consumers about the option of bringing their own containers for takeout food and beverages, at no extra charge. This necessitates operational readiness to handle customer-provided containers hygienically and efficiently.

Mandatory Reusable Takeaway Options (by February 2028)

Complementing the “bring your own” initiative, businesses must, by February 2028, provide and inform consumers about a reusable takeaway container option, also at no extra charge. This could involve deposit-return schemes or subscription models, pushing procurement towards managing a fleet of durable, food-grade reusable containers.

National Adaptations and Fees

While the directive sets EU-wide standards, Member States retain some flexibility in implementation and can introduce additional measures. For example, countries like Spain aim for a 50% reduction in single-use plastic by 2026 and 70% by 2030 by weight, compared to 2022 data. Such national targets create a patchwork of regulations that procurement must navigate, highlighting the need for a pan-European strategy with local adaptability.

Driving a Circular Economy

The overarching goal of these regulations is to drive a truly circular economy for plastics. The EU Single-Use Plastics Directive is projected to yield substantial environmental benefits, including a reduction in greenhouse gas emissions by 2.63 million tonnes annually and a decrease in marine pollution from single-use plastics by 4,850 tonnes per year. This commitment to sustainability offers a powerful narrative for businesses to connect with environmentally conscious consumers and stakeholders.

The future of foodservice procurement lies in embracing reusable systems and adapting to national regulations to drive a circular economy.

Conclusion: Future-Proofing Foodservice Procurement

The EU Single-Use Plastics Directive, along with the subsequent Packaging and Packaging Waste Regulation, is not merely a collection of environmental regulations; it is a profound strategic shift that redefines operational excellence and competitive advantage for foodservice procurement. By proactively embracing sustainable alternatives, integrating robust reusable packaging systems, and adapting to evolving Extended Producer Responsibility schemes, businesses can unlock significant operational efficiencies, stabilize costs, and mitigate regulatory risks.

Beyond compliance, this transformation offers an unparalleled opportunity to enhance brand reputation, attract and retain customers, and secure a resilient, profitable future. Companies that demonstrate strong sustainability leadership will differentiate themselves in a crowded market, translating environmental responsibility into tangible business value and market share opportunity. Reducing reliance on fluctuating fossil plastic costs and optimizing logistics through lighter, more compact sustainable options or reusable systems can lead to substantial long-term cost savings.

Proactive compliance with EU SUPD future-proofs foodservice procurement, enhancing brand, profitability, and environmental legacy.

Act Now for a Sustainable Future

Review your current procurement strategies and align with the EU Single-Use Plastics Directive to build a resilient, compliant, and sustainable supply chain. Explore innovative solutions likeKaffebanerstråand otherbæredygtige boba-halmalternativerto lead the market. Don’t wait for the next regulatory deadline; transform your operations today to secure your competitive edge and environmental legacy. For comprehensive details on the directive, refer to theofficial EU information. You can also find valuable insights from industry experts atAranca on the directive’s implications. For a deeper dive into the broader regulatory landscape, consider exploring resources fromRethink Plastic Alliance.Contact Us for a Compliance Assessment