シニアB2Bの持続可能性コンテンツストラテジストによる

2021 年 7 月に制定された欧州連合の使い捨てプラスチック (SUP) 指令 (指令 2019/904/EU) は、食品サービス部門に重大な影響を与える環境政策の地殻変動を表しています。この指令は単なる規制の更新をはるかに超えたもので、プラスチック汚染、特に SUPD の施行前には全海洋ゴミの最大 70% を占めていた海洋ゴミの蔓延する問題を抑制するために設計された戦略的命令です。調達マネージャー、オペレーションディレクター、サステナビリティ責任者、サプライチェーン幹部にとって、SUPD は単なるコンプライアンスチェックリストではありません。それは、調達、運営、長期的なビジネス戦略を根本的に再評価する必要があるということです。

SUPD の命令を無視するという選択肢はもはやありません。コンプライアンス違反による経営上および商業上の影響は、高額の罰金やサプライチェーンの混乱から、重大な風評被害や環境意識の高まる消費者層の離反に至るまで、深刻です。積極的な適応は、法令順守だけでなく、市場アクセスの確保、ブランド価値の向上、急速に進化する欧州情勢における持続可能な成長の促進にとっても不可欠です。

EU SUPD はフードサービスにとって戦略的必須事項であり、コンプライアンスと持続可能な成長のための積極的な適応が求められています。

EU 使い捨てプラスチック指令の中核原則を理解する

SUP 指令の核心は、環境への影響が高い特定のプラスチック品目を対象とすることで、循環経済への移行を加速することを目的としています。その定義と禁止事項を理解することが、効果的な調達への第一歩です。

使い捨てプラスチックの定義

この指令では、使い捨てプラスチックを、PLA などのバイオプラスチックを含む、廃棄前の 1 回または短期間のみ使用することを目的とした、全体または一部がプラスチックで作られた製品であると正確に定義しています。この広範な定義により包括的な適用範囲が保証され、何が規制に該当するかについて曖昧さの余地がありません。

完全な禁止 (2021 年 7 月 3 日発効)

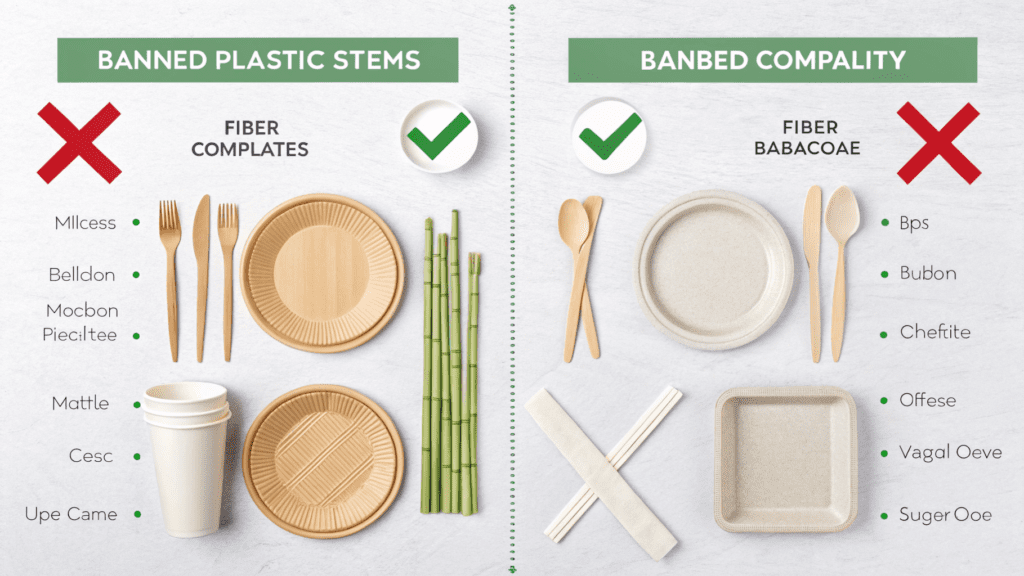

食品サービスの調達に最も直接的な影響を及ぼしたのは、いくつかの一般的な使い捨てプラスチック製品の完全禁止でした。 2021 年 7 月 3 日以降、EU はプラスチック製のカトラリー、皿(PE や PLA などのプラスチックの裏地が付いているものを含む)、ストロー(自力で摂取できない患者のための病院での医療用を除く)、飲料マドラー、綿棒スティック、風船スティック、および発泡ポリスチレン(EPS)製の使い捨て食品容器の市場への出品を禁止しています。さらに、真に持続可能な代替品への取り組みを反映して、オキソ分解性プラスチックで作られたすべての製品は EU 全体で広く禁止されています。

SUP 指令は、影響の大きいプラスチック製品を対象としているため、食品サービスのコンプライアンスに関する定義と禁止事項を明確に理解する必要があります。

食品サービスの調達への直接的な影響: 持続可能な代替品への移行

全面的な禁止により、EU内で営業する外食産業は即時かつ決定的な重大な移行が必要となる。調達チームは、従来のプラスチックから新世代の持続可能な代替品に方向転換する必要があります。

即時的な物質的移行

企業は現在、裏地のない紙、成形繊維、竹、皮、バガス/コーンスターチ、ヤシの葉やアレカなどのその他の植物由来の材料で作られた商品を調達しています。この変化は単に代替品を見つけることではなく、新しい材料哲学をサプライチェーン全体に統合することを意味します。たとえば、革新的な次のようなオプションを検討します。コーヒーグラウンドストローユニークな顧客エクスペリエンスを提供しながら、企業が持続可能性の目標を達成できるよう支援します。

消費量削減目標(2023年~)

この指令は、完全な禁止に加えて、加盟国に対し、使い捨てのプラスチックカップや持ち帰り用容器の消費量を量的に削減することを義務付けている。 2023年以降、各国は2022年の消費レベルをベースラインとしてこれらの削減目標を実施し、2026年までに「目に見える量的削減」を目指す必要があります。これには、材料の代替だけでなく、廃棄物削減の戦略や、場合によっては再利用可能なシステムへの移行も必要です。

PFAS および化学物質の制限 (2026 年 8 月まで)

食品包装の状況は、「永遠の化学物質」を目的とした新しい包装および包装廃棄物規制 (PPWR) によってさらに複雑になっています。この規制により、2026 年 8 月 12 日までに、食品包装中の 25 ppb (ppb) を超えるパーフルオロアルキル物質およびポリフルオロアルキル物質 (PFAS) を対象とした PFAS 分析が禁止されます。この厳しい制限により、すべてのバリア コーティングと食品と接触する材料の徹底的な見直しが必要となり、重大なコンプライアンス リスクを回避するために PFAS フリーのソリューションへの調達が推進されます。

農産物におけるプラスチックの廃止(2030年1月まで)

PPWR は生鮮食品にも範囲を広げています。 2030 年 1 月 1 日より、水分損失や微生物学的危険の軽減などの特定のニーズに対する限定的な例外を除き、重量 1.5 キログラム (kg) 未満の未加工の生の果物と野菜の使い捨てプラスチック包装が禁止されます。この将来の禁止には、農産物のサプライチェーンと包装開発における先見の明が必要です。

食品サービスの調達では、持続可能な素材に移行し、削減目標を達成し、PFAS に備えてプラスチック禁止を推進する必要があります。

Evolving Compliance & Operational Shifts Under the EU Single-Use Plastics Directive

SUPD の影響は材料組成を超えて、ラベル表示、生産者の責任、製品デザインにまで及びます。

表示義務(2022年7月以降)

SUPD では透明性が重要です。 2022 年 7 月以降、EU で販売されるすべての使い捨てカップには、水性の裏地が付いているものであっても、目立つ、はっきりと読み取れる、消えない「Plastic in Product」または「Made of Plastic」のカメのロゴを表示する必要があります。このマーキングは、プラスチックの含有量、環境への影響、適切な廃棄方法を消費者に知らせ、消費者の認識と廃棄行動に直接影響を与えます。

拡大生産者責任 (EPR) 制度 (2024 年 12 月 31 日から)

「汚染者負担」の原則は SUPD の基礎です。 2024 年 12 月 31 日より、生産者は、食品容器、パケット、包装紙、飲料容器、カップ、軽量ビニール袋を含む特定の SUP 品目の収集、輸送、処理、ゴミの清掃、意識向上措置に対する経済的責任を負うことになります。これらの EPR スキームはパッケージングのコスト構造を根本的に変え、持続可能な材料の選択を長期的には経済的に魅力的なものにします。

付属キャップとリサイクルコンテンツの目標(2024年7月まで)

この指令は、リサイクル性を促進するための製品設計にも言及しています。 2024年7月から、3リットルまでの飲料容器にはペットボトルのキャップと蓋の取り付けが義務化され、分別ごみ化が防止されます。さらに、リサイクル含有量の厳しい目標が設定されています。2025 年までにペットボトルには少なくとも 25% の再生プラスチックが含まれなければならず、2030 年までにすべてのペットボトルの 30% に増加します。これにより、リサイクル含有量の需要が高まり、循環経済が強化されます。

回収対象の増加

これらのリサイクル目標を支援するために、この指令はペットボトルの回収率を 2025 年までに 77%、2029 年までになんと 90% とする野心的な目標を設定しています。加盟国は、これらの回収率を達成するために、保証金返還制度を含むさまざまな戦略を実施しています。たとえば、ドイツのデポジット返還システムは、すでにプラスチック飲料ボトルの回収率 98% という驚異的な数字を誇っており、このようなスキームの有効性が実証されています。

SUPD は、ラベル表示、EPR スキーム、付属のキャップ、リサイクルされた内容、およびより高い収集目標を義務付け、食品サービス業務を再構築します。

EUの使い捨てプラスチック指令遵守のための戦略的調達

これらの多面的な規制に対処するには、調達機能の戦略的な見直しが必要です。

サプライヤーの再評価と調達

調達チームの当面の課題は、真に準拠した代替品を提供するサプライヤーを特定し、採用することです。これには、認証(産業用堆肥化規格 EN 13432 など)、材料組成、サプライチェーンの信頼性に関する徹底的な審査が含まれます。企業は、次のような代替手段を確保する必要があります。持続可能なボバストローの代替品、規制要件を満たすだけでなく、運用上の要求や顧客の期待も満たします。

移行によるコストへの影響

コンプライアンスの長期的なメリットは明らかですが、最初の移行ではコストの問題が生じる可能性があります。生分解性または堆肥化可能な製品は、最初はプラスチック製の製品よりも高価になる可能性があります。ただし、これらの初期費用は、コンプライアンス違反による重大なリスク、罰金の可能性、および EPR 料金の削減やブランド価値の向上による長期的な節約と比較検討する必要があります。例えば、ポーランドはすでに2024年1月から廃棄物管理をカバーするために使い捨てプラスチックに追加料金(例:カップには0.20ズウォティ、食品容器には0.25ズウォティ)を適用しており、コンプライアンス違反による直接的な経済的影響を示している。

物流と保管の最適化

より軽量でコンパクトな持続可能な代替品に移行すると、予期せぬメリットが得られる可能性があります。これらの材料は、輸送時の二酸化炭素排出量を削減し、保管ニーズを最適化することができ、倉庫保管と流通における業務効率と潜在的なコスト削減につながります。この最適化は、より機敏で持続可能なサプライ チェーンを構築する上で重要な役割を果たします。

ミニケーススタディ: Xylomatrix の PFAS フリーのイノベーション

コンプライアンス主導のイノベーションの代表的な例は、生分解性セルロース繊維パッケージングを提供する企業 Xylomatrix によるものです。同社のソリューションは、有害な PFAS 化学物質に依存せずに重要な水とグリースのバリアを提供し、今後の PPWR 制限に直接対処します。このようなイノベーションは、企業がどのようにして遵守するだけでなく、より安全で持続可能な製品で市場をリードし、信頼と評判を構築できるかを浮き彫りにします。ヨーロッパの多くの主要な食品サービス事業者はすでに認定された堆肥化可能な包装を要求しており、市場主導の変化を示しています。

比較表: 使い捨てプラスチックと準拠した代替品

| 特徴 | B2B運用上の影響 | コンプライアンスノート | ROIポテンシャル |

|---|---|---|---|

| 使い捨てプラスチックカトラリー(PS/PP) | 廃棄物量が多い。継続的な廃棄コスト。 | 禁止2021 年 7 月から EU 全体 (指令 2019/904/EU)。 | マイナス: 多額の罰金、深刻な風評被害、消費者の反発、市場からの排除のリスク。 |

| 成形ファイバープレート(バガス) | 新しいサプライヤー関係が必要です。単価が高くなる可能性があります。 | 準拠EU で広く受け入れられている代替案。多くの場合、工業的に堆肥化可能です (EN 13432)。 | ポジティブ: ブランドイメージの強化、持続可能性に対する消費者と規制の需要の高まりへの対応、廃棄物管理コストの削減の可能性 (堆肥化可能性など)、将来の禁止を積極的に回避することによる長期的な運用の安定性。循環経済の目標をサポートします。 |

| 使い捨てプラスチックカップ(PET/PP裏地) | 消費削減目標。ラベルの要件。 | 削減目標2023年から。 2022 年 7 月から「Plastic in Product」ラベル。 | 変数: コンプライアンス違反のリスク (罰金、公的監視)。削減イニシアチブによるコスト削減の機会。ブランド認知の向上。再利用可能なオプションへの戦略的移行により、長期的に大幅な節約とより強いロイヤルティがもたらされます。 |

| 再利用可能なコンテナシステム | 洗浄/消毒インフラへの投資。返品のための物流。 | 義務付けられた2030年までにオンサイト化。 2028 年 2 月までにお持ち帰りオプションをご利用いただけます (追加料金なし)。 | 高: 使い捨て製品の繰り返し購入の排除による大幅な長期コスト削減、強力な持続可能性リーダーシップ、顧客ロイヤルティの向上、潜在的な新たな収益源 (デポジット スキーム)、変動する材料コストへの依存の軽減。環境フットプリントを大幅に削減し、ビジネスを持続可能性の市場リーダーとしての地位を確立します。 |

戦略的調達には、サプライヤーの再評価、移行コストの管理、物流の最適化、革新的な準拠ソリューションの採用が含まれます。

Embracing Reusable Solutions & Future Outlook for Foodservice Procurement

SUPD とその後の規制は、使い捨て材料の代替から体系的な変更への移行を強調し、再利用可能なシステムへの強力な推進を明確に示しています。

HORECA における将来の禁止 (2030 年まで)

規制の方向性は明らかです。2030 年までに、ホテル、レストラン、ケータリング施設の敷地内で消費される特定の食品および飲料の使い捨て包装が禁止されます。これは、クリーマー、砂糖のパケット、調味料の小袋などの個別の分量の容器にも当てはまります。この差し迫った禁止により、外食事業者は再利用可能な食器、カトラリー、調味料ディスペンサーへの投資が求められます。

お客様独自のコンテナオプション(2027年2月まで)

再利用の文化を促進するために、外食サービス施設は 2027 年 2 月までに、飲食物の持ち帰り用の容器を追加料金なしで持参するオプションを消費者に提供し、積極的に通知することが義務付けられます。そのため、顧客が用意したコンテナを衛生的かつ効率的に取り扱うための運用準備が必要です。

再利用可能な持ち帰りオプションの義務化 (2028 年 2 月まで)

「Bring Your Own」の取り組みを補完するものとして、企業は 2028 年 2 月までに、再利用可能な持ち帰り用容器のオプションを追加料金なしで提供し、消費者に通知する必要があります。これには、デポジット返還スキームやサブスクリプションモデルが含まれる可能性があり、耐久性のある食品グレードの再利用可能なコンテナのフリートの管理に向けて調達を推進します。

国内適応と料金

この指令は EU 全体の基準を定めていますが、加盟国は実施においてある程度の柔軟性を保持しており、追加措置を導入することができます。たとえば、スペインのような国は、2022年のデータと比較して、使い捨てプラスチックを重量で2026年までに50%削減、2030年までに70%削減することを目標としています。このような国家目標は、調達が対応しなければならない規制のパッチワークを生み出し、地域の適応性を備えた汎欧州戦略の必要性を浮き彫りにしています。

循環経済の推進

これらの規制の最も重要な目標は、プラスチックの真の循環経済を推進することです。 EU の使い捨てプラスチック指令は、温室効果ガス排出量を年間 263 万トン削減し、使い捨てプラスチックによる海洋汚染を年間 4,850 トン削減するなど、環境に大きなメリットをもたらすと予測されています。持続可能性へのこの取り組みは、企業が環境に配慮した消費者や関係者とつながるための強力な物語を提供します。

食品サービス調達の将来は、再利用可能なシステムを採用し、循環経済を推進するための国の規制に適応することにあります。

結論: 将来を見据えたフードサービス調達

EU 使い捨てプラスチック指令とそれに続く包装および包装廃棄物規制は、単なる環境規制の集合体ではありません。これは、食品サービス調達におけるオペレーショナルエクセレンスと競争上の優位性を再定義する、根本的な戦略的転換です。持続可能な代替品を積極的に採用し、堅牢で再利用可能な包装システムを統合し、進化する拡大生産者責任スキームに適応することで、企業は大幅な業務効率を実現し、コストを安定させ、規制リスクを軽減することができます。

この変革は、コンプライアンスを超えて、ブランドの評判を高め、顧客を引き付けて維持し、回復力と収益性の高い未来を確保する比類のない機会を提供します。サステナビリティに関する強力なリーダーシップを発揮する企業は、環境への責任を目に見えるビジネス価値と市場シェアの機会に変え、混雑した市場で差別化を図ることができます。変動する化石プラスチックのコストへの依存を減らし、より軽量でコンパクトな持続可能なオプションや再利用可能なシステムを通じて物流を最適化することは、長期的な大幅なコスト削減につながる可能性があります。

EU SUPD への積極的な準拠により、将来性のある食品サービスの調達が実現し、ブランド、収益性、環境遺産が強化されます。

持続可能な未来のために今すぐ行動しましょう

現在の調達戦略を見直し、EU の使い捨てプラスチック指令に準拠して、回復力があり、準拠した持続可能なサプライ チェーンを構築します。次のような革新的なソリューションを検討してくださいコーヒーグラウンドストローその他持続可能なボバストローの代替品市場をリードするために。次の規制期限を待つ必要はありません。競争力と環境遺産を確保するために、今すぐ業務を変革しましょう。この指令の包括的な詳細については、以下を参照してください。EUの公式情報。業界の専門家からの貴重な洞察も次のサイトで見つけることができます。アランカ氏、指令の意味について語る。より広範な規制状況をさらに詳しく調べるには、次のリソースを検討してください。プラスチック同盟を再考する。コンプライアンス評価についてはお問い合わせください